Another conflict. Another headline cycle. Pakistan threw its usual tantrum. We stayed calm, and this time, we showed them.

200+ drones. Neutralised overnight. Missiles? Shot down. Our own version of the Iron Dome? Tested. Live. Not in a lab. Not on a PowerPoint.

This wasn’t just defense. It was a product demo for the world.

India’s defence tech isn’t just ready. It’s market-ready. And unlike China’s systems, the ones Pakistan used, ours actually work.

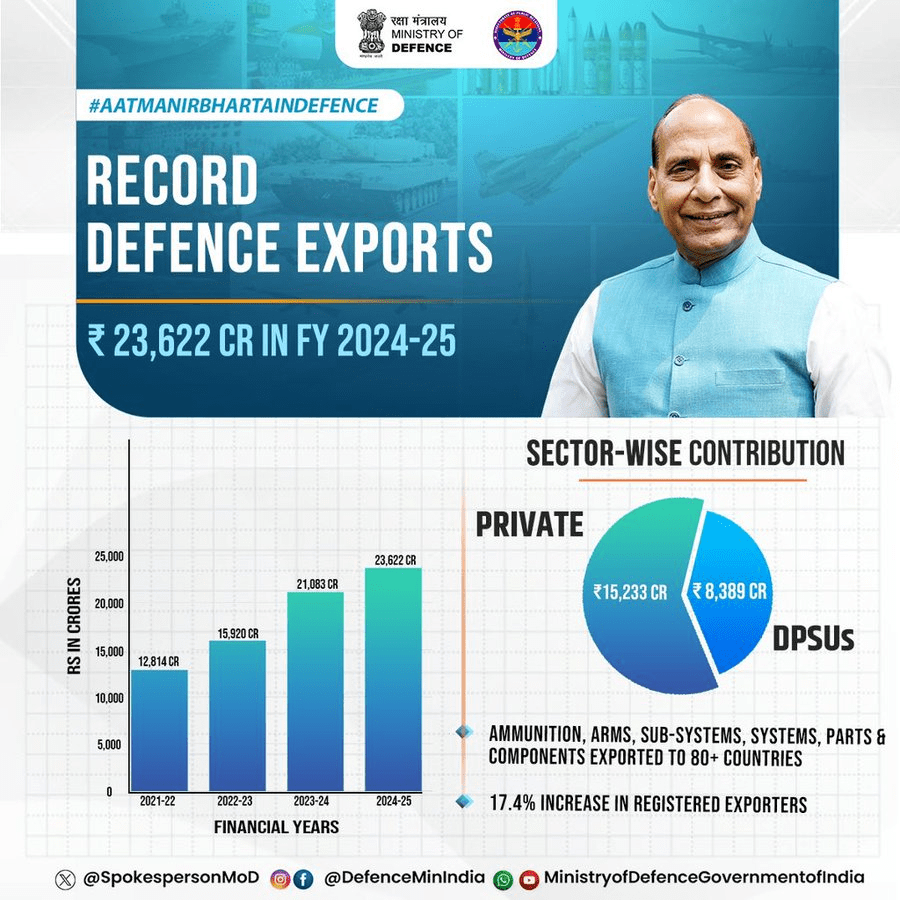

India’s defense exports has already got the momentum. In 2017 our defense export was around ₹1521 Crore. And now in 2025, exports are up to ₹23600 Crore.

Its poised to go up and up after this.

But here’s the thing. This war shouldn’t define us. It should wake us up. Because we already know how to handle Pakistan.

We bleed them slowly. Quietly. “Unknown man kills a terrorist” — that’s the headline we aim for. Keep hitting their roots till their morale hits rock bottom. So that when the day comes, and we really announce an attack, Pakistani soldiers abandon their border posts and run for their lives.

That’s how you take down a rogue state — by weakening it from within. Not by reacting, but by outgrowing.

Pakistan is not the goal. China is.

I remember reading a line from a Pakistani journalist when our businessmen visited Pakistan for some event few decades back.

“We don’t fear India’s new weapons. We fear the day Indian billionaires land in Islamabad in their private jets.”

That’s the power we need to chase. The kind that doesn’t just win battles, but dominates boardrooms.

We don’t need another border skirmish. We need GDP growth. We need billion-dollar IPOs. We need our own Nvidia, our own Tesla, our own AI giants.

Let’s not waste time chasing a neighbour stuck in the past. Let’s build. Let’s sell. Let’s grow. And when the world talks about superpowers in 2040, let’s make sure India isn’t just on the list. It leads it.

Let’s start with a simple question — when you open a savings account, who do you think is doing a favor? You, by trusting them with your money? Or them, by “letting” you be their customer?

If you said “them,” congratulations, you just described the Indian banking system’s mindset.

How Indian Banks Are Robbing You Silently

Let’s talk about facts, not feelings.

According to a report from The Hindu Business Line, public sector banks (PSBs) alone collected around ₹8500 crore between FY20 and FY24 just by penalizing people for not maintaining minimum balance.

Yes, you read that right.

In the middle of a pandemic, inflation, job cuts — our “saviours” were busy fining people for not keeping enough money in their accounts. The same people who probably couldn’t make ends meet were slapped with penalties because their account balance wasn’t up to the banks’ “standards.”

Imagine punishing a drowning man for not swimming properly.

And it doesn’t end there.

As per another report by Moneylife, banks have written off ₹1.635 lakh crore of bad loans in just the past ten years.

You and I are being fined for not keeping ₹5000 in our account. Meanwhile, the big boys — companies and corporates — default on crores, and the banks just “write it off.” It’s like you lending money to someone, they ghost you, and you just shrug and say, “Forget it.”

But if your balance falls by ₹50, you’re a criminal in their eyes.

Who Are Banks Actually Working For?

It’s clear — banks in India seem to work for the big corporates, not the common man.

They squeeze the small guy dry with penalties, fees, hidden charges, service tax, and then calmly “forgive” massive loans of rich borrowers. No follow-ups. No stress. No shame.

And you know what’s worse?

Despite this robbery model, they are still some of the “top” companies in India.

Compare This: India vs USA

Let’s look at the latest top 10 companies by market cap.

US Top 10 (April 2025):

Apple

Microsoft

Nvidia

Alphabet (Google)

Amazon

Meta (Facebook)

Berkshire Hathaway

Eli Lilly

Broadcom

Exxon Mobil

Almost all are tech, innovation, or healthcare-driven, except Berkshire and Exxon.

India Top 10 (April 2025):

Reliance Industries

TCS (Tata Consultancy Services)

HDFC Bank

ICICI Bank

Infosys

Bharti Airtel

State Bank of India (SBI)

Kotak Mahindra Bank

ITC

Bajaj Finance

Notice something?

Banks everywhere.

The US top companies are inventing the future. Our top companies are collecting EMIs, charging penalties, and funding “write-offs.” This is the sad reality.

What’s the Cost to Us?

This system discourages savings, hurts financial literacy, and makes the common person feel small and helpless.

Instead of rewarding savers, supporting small businesses, or investing aggressively into tech, innovation, or manufacturing — our banking system is busy building castles of “service charges” and “processing fees” on the backs of regular citizens.

Banks were supposed to be pillars of trust. Instead, they have become legalized mafia, operating behind a curtain of regulation.

Time for a Wake-Up Call

The next time you hear a politician or a banker talk about “financial inclusion,” remember — the same system is designed to profit off your struggle.

The same system that fines you for being poor and forgives billionaires for being reckless.

Maybe it’s time we start questioning not just bad governance but also bad banking.

Because if banks are supposed to be the backbone of our economy, ours are busy breaking it, one penalty at a time.

Stay aware. Stay woke. Protect your money — because clearly, no one else will.

Right now, I’m writing this sitting in Malkapur – my hometown. Tucked near the border of Madhya Pradesh, right in the heart of Maharashtra, this small town has always held a simple, quiet charm for me. But this time, something feels different.

Summer has arrived, and with it, the brutal reality of rising temperatures. As I walk through familiar streets, I can’t help but notice how people are adapting to survive the heat. Almost every house now has an air conditioner or, at the very least, a water cooler. Honestly, I can’t imagine a home here without one.

Green cloths and makeshift covers hang across balconies, terraces, and windows – a desperate but clever attempt to block the ruthless sunlight from turning homes into furnaces. It’s not just about comfort anymore.

It’s about survival.

Water scarcity is another daily battle. With an unreliable water supply during summer, people have turned to large storage tanks stacked atop their buildings. It’s a common sight now, as essential as the walls that hold the homes together.

As I sit here at 6:20 p.m., during the last week of April, the temperature outside is still hovering around 37°C. It goes up to 43°C at peak time and even at 3:00 a.m night time., when the world should feel a little cooler, it barely drops to 27°C.

That’s the harsh reality today.

And honestly, it’s crazy when I think about how things used to be.

I remember a time – just 10 years back – when we used to play cricket till noon under the summer sun. Sure, it was hot back then too, but it was manageable. We never even thought twice about it.

Today, stepping out after 10 a.m. for a simple game feels unthinkable. The heat isn’t just uncomfortable anymore – it feels dangerous.

This rising temperature wave isn’t just making summers tough. It’s starting to affect livelihoods.

Daily wage workers, street vendors, construction workers – they now avoid working between 12 to 5 p.m., because it’s almost impossible to function in that kind of heat. Work slows down, incomes shrink, and the struggle only gets harder.

But amidst these challenges, there’s a silver lining.

I noticed something heartening – greenery.

More trees. More plants. It seems people have realized the old wisdom: plant more trees, get more rain. In fact, Malkapur looks much cleaner and greener compared to three or four years ago. It feels like a town trying to breathe again, trying to heal itself in small but significant ways.

Yet, a question lingers in my mind – will these efforts be enough? Will planting trees, covering windows, and storing water really solve the larger problem of rising temperatures year after year?

Or are we just buying time, without addressing the root causes?

This is a question not just for Malkapur, but for every small town grappling with the harsh face of climate change.

Let’s face it. Investing looks cool when your portfolio is all green, but staying consistently profitable? That takes a bit of homework, a pinch of discipline, and a good eye for fundamentals.

Here are some investing rules that have helping me stay sane and grow my portfolio steadily, even when markets acted like a moody teenager.

Read the Damn Concall

Before you get tempted by a trending stock or a flashy YouTube thumbnail promising “Next Multibagger,” do this:

Go to the company’s Annual Report. Read the Management Discussion and Analysis.

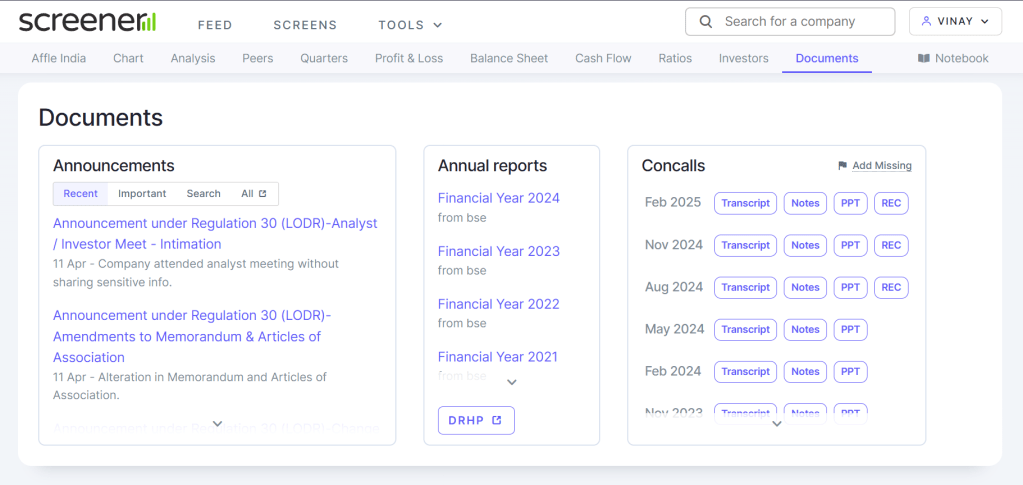

Even better? Catch the quarterly concalls. Use tools like Screener.in. You can download concalls transcript from there. Concalls tell you what the company is actually planning, not what influencers are hyping.

Screenshot from screener.in – Documents/ Reports section

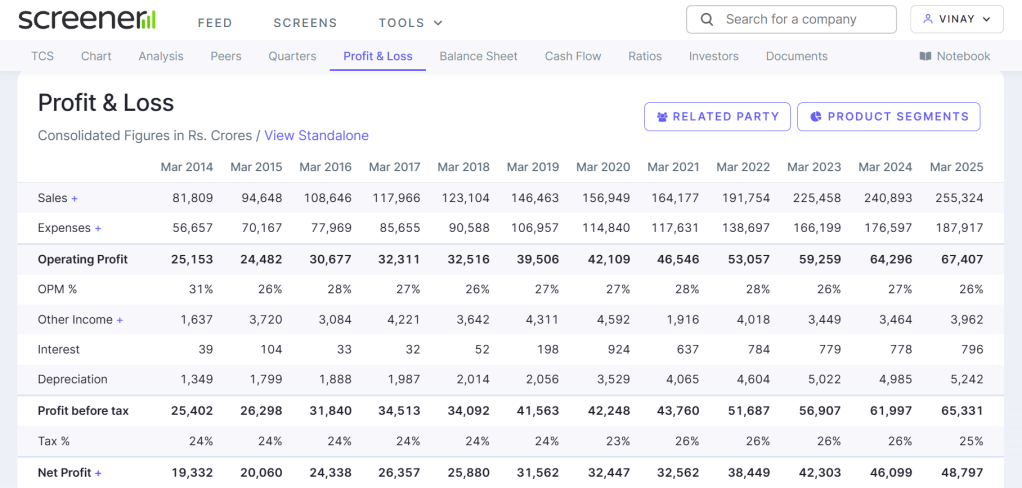

The company’s financial data are goldmines for more context on how company is really doing. Make sure company is consistently growing in terms of revenue and Profits.

Screenshot from screener.in – Profit and Loss section

Avoid Stocks With Sky-High PE (Unless You Love Pain)

If a stock’s Price to Earnings ratio is flying at 200 to 400+, ask yourself if you’re investing or just buying FOMO.

PE ratio = stock price divided by the company’s earnings per share.

It tells you how much people are willing to pay for each rupee of the company’s profit.

A high PE means the stock is priced for big future growth. But when the hype fades or growth slows, these stocks often crash harder than your New Year resolutions.

Valuations matter. There’s a reason even the best businesses crash when priced like they’ll change the world every quarter.

Believe in the India Story (But Don’t Be Blind)

India’s massive population and growing consumer base mean we’re just getting started. There’s still a long runway ahead… more people entering the workforce, rising incomes, urban expansion, digital adoption. All of it signals economic progress in motion.

And that’s the opportunity. We’re not just spectators; we can ride this growth if we pick the right players.

But don’t get carried away. Just because a company has “India” in its tagline doesn’t make it invest-worthy.

Do your homework. Compare revenue, profit margins, debt, and ROE. Let fundamentals guide your bets… not blind optimism. Also, don’t marry your stocks. Winners change. Rotate when the data tells you to.

Winners Deserve Your Trust (And Your Capital)

If a stock in your portfolio has outperformed others, don’t just clap, add more. Ride the momentum. Winners often keep winning until they don’t.

Which brings me to…

Know When to Cut and Run

Stock at all-time high for no clear reason? Take some profits.

Company posts a bad quarter and management sounds confused? Cut your position.

This is not emotional. This is maintenance. Just like you clean your room (hopefully), you clean your portfolio.

What’s Down? What’s Cheap? Investigate It.

When everyone’s running away from an asset, that’s when you pay attention.

Is it down because of a short-term trend or long-term trouble?

Are the fundamentals still solid?

If yes, and the price is at a discount, go in like it’s free cake with chocolate on top.

Selling? Do It Smartly

If an asset is booming and you feel like it’s overvalued, don’t wait for a crash.

Take profits in slices. Maybe sell 10 to 20 percent of your position. This way, you secure gains and stay in the game in case it still runs.

KISS (Keep It Simple, stupid!)

Most successful investing strategies are boring. They don’t involve 17 indicators and 9-hour screen time. They involve:

Knowing what you own

Tracking performance

Making data-driven decisions

If you’re just guessing, you’re gambling. Might as well head to Goa.

Investment Avenues for Indian Investors

Here’s where you can put your money to work:

Indian Stock Market (Equities, Mutual Funds, ETFs)

US Stock Market (via INDMoney, Vested, etc.)

Gold and Silver (SGBs, ETFs, physical)

Crypto (risky but rewarding if done right)

Each of these plays differently in market cycles. Rotate and rebalance based on trends, valuations, and your risk appetite.

Final Word

This isn’t about timing the market perfectly. It’s about building habits that stack the odds in your favor.

If you’re willing to put in the work, just like you do for your gym gains or side hustle, investing can become your greatest wealth-building engine.

So here’s a question for you: What’s one investing mistake you wish you never made?

Drop it in the comments or shoot me a DM. Let’s learn and grow together.

Elon Musk used first-principle thinking to solve complex real-world problems at Tesla and SpaceX. I read about it, tried to simplify it and understand how we can use the same approach in our lives.

What’s first principle thinking?

First-principles thinking is like taking a problem apart to its most basic pieces, ignoring what everyone else says or does, and building a solution from scratch based on what’s absolutely true.

It’s about asking, “What do we know is true?” and starting there instead of copying what’s already out there.

To apply this in our lives, you will have to start questioning common advice and beliefs.

Don’t just accept “this is how it’s done” (e.g. “you need a college degree to succeed” or “work 9-to-5 for 40 years”). Ask why those rules exist and if they make sense for you.

Example in Life:

You’re told to buy a house because “it’s a good investment.”

Instead, break it down:

What’s a house? A place to live that costs money (home loans, taxes, maintenance).

What’s the goal? Financial security and comfort.

Truth: Renting might be cheaper and give flexibility if you move often. So, you calculate costs and decide renting aligns better with your goals.

Example in Career:

Everyone says “climb the corporate ladder.” But you ask: What’s a career? A way to earn money and find purpose.

Truth: Freelancing or starting a side hustle could give you more control and fulfilment. You test it by learning a skill like coding or design, skipping the traditional path.

Elon Musk used the first principles at Tesla.

He didn’t just accept that batteries were pricey. He looked at the raw materials, calculated their cost, and figured out Tesla could make batteries cheaper by building their own factories (like the Gigafactory). This helped Tesla make electric cars more affordable over time.

How You Can Start

Start questioning everything. Next time someone says “That’s just how it’s done,” ask: “Why?” “What’s the goal here?” “Is this actually true for me?”

You don’t need to be Elon to think like him. You just need curiosity, courage, and the willingness to start from scratch.